Table of Contents

- US FEDERAL TAX CALCULATION

- Federal Tax Calculation

- General Set Up

- IPUTP - Federal Tax Parameters

- IPUTR - Federal Tax Rates

- IPRLU - US Tax Filing Information

- Federal PC Usages

- PC Usage - Federal Tax

- PC Usage - Federal Insurance Contribution Act (FICA) Tax

- PC Usage - Medicare Tax

- PC Usage - Federal Unemployment Tax Act (FUTA)

- PC Usage â Railroad Taxation

- Federal Tax Calculation

- UPCALC Example - Federal Withholdings

- FICA / MEDICARE

- FICA Wage < FIT Wage Example

- Railroad Tax Calculation

- Railroad â Tier1 Tax Example

- Notes

US FEDERAL TAX CALCULATION#

Federal Tax Calculation#

General Set Up#

- UDGNIS

- This is the process to load all US Tax Jurisdictions into IDCO, IDSP, IDCN, IDCI, IDMN, IDSD, IDZR, and IDTX.

- UPUTR

- This is the process to load all US Tax Rates and States Miscellaneous Parameters. After UPUTR is run, IPUTR and IPUTP screens can be used to view the applicable Tax Rates and Miscellaneous Parameters by state.

- IPUTR

- US Tax Rates may be viewed by state and overridden Rates and Wage Base may be entered. Some SUTA surcharge calculation for some states may be suppressed by checking the 'Do not Calculate' toggle.

- IPUTP

- US Tax Miscellaneous Parameters may be viewed by the states that are applicable for the IPRLU screen.

- IDGV

- This screen may optionally contain specific override Rates and Wage Bases by Government Registration for each registration from the pay header's group. IDGV overridden amounts take precedence over the IPUTR overridden amounts.

- IDTX

- This screen is used to enter applicable Tax Jurisdictions that are paid by employees. On screens such as IPPH/IEPI, IEAS, IDLN, etc. that require a Tax Jurisdiction, the 'Tax Jurisdiction Editor Utility' dialog box can be used to enter the jurisdiction on the IDTX screen.

- IPRLU/IPRULS

- Each employee must be set up with the applicable tax methods. Miscellaneous Tax Parameters must be set up by the states that need to be paid.

- UPRLU

- This process audits the US Tax Filing information and generates IPRLU Miscellaneous Tax Parameters information according to the IMCT set up.

- The Pay Header tab must specify the default work and home jurisdictions.

- Within the Pay Lines tab, the Jurisdiction field must specify the work jurisdiction of this pay line.

- After a trial calc or having run UPCALC, the Pay Amounts tab will contain, in summary, all the US Taxation amounts that are used for the calculation of net pay.

- The Pay Jurisdiction tab contains the default Work and Home jurisdictions.

- After a trial calc or having run UPCALC,the Pay Jurisdiction tab will contain, in detail, all the US Taxation amounts by jurisdiction.

IPUTP - Federal Tax Parameters#

When UPUTR is run, it loads in a list of the Federal tax parameters for the Symmetry Federal Tax calculation.On the IPUTP screen, the following Federal tax parameters are available to be used on the IPRLU/IPRLUS screen:

- 401K_CATCHUP

- IRS_MAX_EXEMPTIONS

- 401K_CATCHUP

- Optional, character, 401K Limit Catch Up Option

- Indicates to Symmetry if the employee is enrolled in a 401k Catch Up plan

- The annual regular 401k contribution limit is defined by the IRS (e.g. $16,500). If an employee is enrolled in a 401k plan with annual contribution limit greater than this regular limit, this parameter will allow the 401k maximum contribution to exceed the IRS limit for Benefit Pre-tax calculation.

- Options:

- 'DEFAULT'-Catch Up is not allowed

- 'YES'-Catch Up is allowed

- 'NO'-Catch Up is not allowed

- If 401K Catch Up option is applicable to all employees, 'YES' can be entered in the IPUTP default value, otherwise each employee can specify the value for this option on the IPRLU/IPRLUS screen.

- IRS_MAX_EXEMPTIONS

- Optional, numeric, IRS maximum number of exemptions allowed

- Allows an employer to indicate on the employee's IPRLU/IPRLUS screen, the maximum number of exemptions allowed for this employee as indicated by the IRS in a 'lock-in-letter'

- UPCALC will cap the employee's federal '# of exemptions' with the value from the IPRLU/IPRLUS 'IRS_MAX_EXEMPTIONS' parameter

- Do not provide a default value for this parameter

- Any number provided will override the Federal Exemptions defined in the Federal Tax

IPUTR - Federal Tax Rates#

When UPUTR is run, it loads in a list of federal tax rates for Symmetry Federal Tax calculation.- On the IPUTR screen, set the State field to 'Federal' in order to view the federal tax rates.

- Each Tax Identifier may provide the default Tax Rates, Wage Base to be used for Federal Tax calculation

IPRLU - US Tax Filing Information#

Both the IPRLU and IPRLUS screens can be used to maintain US tax filing information for an employee.

- IPRLU

- Contains all US tax filing information for both Vertex and Symmetry Tax users

- IPRLUS

- Contains US tax filing information for Symmetry Tax users only

- The Federal, State and local tabs must specify all the tax methods and eligible information.

- For Federal Tax calculation, the '# of Exemptions' must be entered on the Federal tab, if the employee has an IRS letter to indicate the maximum number of exemptions they are allowed. The Misc. Identifier field is then set to 'IRS_MAX_EXEMPTIONS' on either the IPRLU Miscellaneous tab or the IPRLUS State tab. Any number provided will override the Federal Exemptions, including a value of 0.

Federal PC Usages#

PC Usage - Federal Tax#

On the IPPC screen, set up pay components for the following PC Usages used in federal tax calculation:| Usage | Description |

|---|---|

| 6001 | FWT Deduction - Regular Tax |

| 6002 | FWT Deduction - Additional Tax |

| 6003 | FWT Deduction - Supplemental Tax |

| 6004 | FWT Earnings - Regular Tax |

| 6005 | FWT Earnings - Regular Tax |

| 6051 | Pre-FWT Earnings - Reg Tax Table Method (PPE) |

| 6052 | Pre-FWT Earnings - Reg Tax % Method (PPE) |

| 6053 | Pre-FWT 125 Exemption - Reg Tax (PPE) |

| 6054 | Pre-FWT 401K Exemption - Reg Tax (PPE) |

| 6055 | Pre-FWT Earnings - Supplemental Tax (PPE) |

| 6056 | Pre-FWT 125 Exemption - Supplemental Tax (PPE) |

| 6057 | Pre-FWT 401K Exemption - Supplemental Tax (PPE) |

| 6058 | Pre-FIT Hours - Total Hours worked (PPE) |

| 7901 to | Pre-FWT 125 Exemption - Reg Tax (PPE) |

| 7928 | Pre-FWT HSA Exemption -Suppl Tax (PPE) |

| 7801 to | Pre-Reg Custom Benefit 01 - Reg Tax (PPE) |

| 7830 | Pre-Sup Custom Benefit 10 - Suppl Tax (PPE) |

PC Usage - Federal Insurance Contribution Act (FICA) Tax#

Federal Insurance Contributions Act Tax (FICA) is imposed by the federal government on both employees and employers. The FICA tax is calculated using Pay Component Usages 6201 - 6261.| Usage | Description |

|---|---|

| 6201 | FICA Employee Deduction |

| 6202 | FICA Employee Earnings |

| 6210 | FICA Employer Contribution |

| 6211 | FICA Employer Earnings |

| 6251 | Pre-FICA Employee Earnings (PPE) |

| 6261 | Pre-FICA Employer Earnings (PPE) |

PC Usage - Medicare Tax#

Medicare tax is an employer and employee paid tax. The Medicare tax is calculated using Pay Component Usages 6501 - 6552.| Usage | Description |

|---|---|

| 6501 | Medicare Employee Deduction |

| 6502 | Medicare Employee Earnings |

| 6503 | Medicare Employer Contribution |

| 6504 | Medicare Employer Earnings |

| 6551 | Pre- Medicare Employee Earnings (PPE) |

| 6552 | Pre- Medicare Employer Earnings (PPE) |

PC Usage - Federal Unemployment Tax Act (FUTA)#

Federal Unemployment Tax Act (FUTA) is an employer paid tax. The FUTA tax is calculated using Pay Component Usages 6401 - 6451.| Usage | Description |

|---|---|

| 6401 | FUTA Employer Contribution |

| 6402 | FUTA Employer Earnings |

| 6451 | Pre-FUTA Employer Earnings (PPE) |

There are two ways of providing the FUTA tax rate:

- IPUTR

- Enter the Rate or Wage Base provided by the government into the appropriate override fields

- These overrides are applicable for the entire company for the federal calculations

- IDGV

- If there is a specific rate given by the government for different Registration #, then enter on IDGV by 'Reg Type', this overrides the IPUTR Rate

- UPCALC retrieves IDGV by Government Registration from Employee's Pay Header Group

If you do business in a state that has been given a FUTA Tax Credit reduction, the new FUTA tax rate for that particular state may be entered in IDGV for the state. In IDGV add a new entry for the specific state, select Registration Type âUS SUI Regist 1â, the Govt Rate Type should be âUS FUTA Rateâ. This state specific FUTA rate will be picked up by the UPCALC program when an employee is being paid in that state.

PC Usage â Railroad Taxation#

PC Usages 6301 â 6356

Federal Tax Calculation#

UPCALC Example - Federal Withholdings #

US Federal Tax Calculation_01.JPG

| IPRLU Federal Filing Status | Single |

| Regular Earnings | 1923.08 |

| Supplemental Earnings | 100.00 |

- Pre-Tax Benefits

- Prorate Pre-Tax Benefits to Regular and Supplemental Earnings

| Reg Earn Pre-Tax Benefit | 1923.08 / 2023.08 * 310.42 = 295.08 |

| Sup Earn Pre-Tax Benefit | 100 / 2023.08 * 310.42 = 15.34 |

- FIT Withholding

| PC 8005 FIT Earn | 1923.08 â 295.08 = 1628.00 |

| PC 8015 FSP Earn | 100.00 â 15.34 = 84.66 |

| PC 6000 FIT Tax | Based on PC 8005 $1628.00 = 237.77 |

| PC 6010 FSP Tax | Based on PC 8015 $84.66 x 25% = 21.17 |

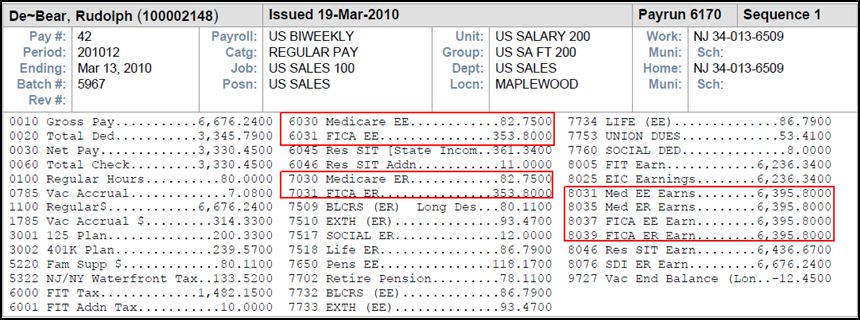

FICA / MEDICARE#

FICA Wage < FIT Wage Example#

US Federal Tax Calculation_02.JPG

Employee works for Regular Employment and Railroad Employment. FICA YTD and RRTA YTD are both used in FICA Calculation.

| FIT_Wages | Usage 6051 Pre FWT Earnings | 6676.24 |

| FICA_Wages | Usage 6261 Pre-FICA Employer Earnings | 6596.13 |

| PC 8005 FIT Earn | =FIT_Wages â 125 - 401K | = 6676.24 â 200.33 â 239.57 | = 6236.34 |

| PC 8039 FICA ER Earn | =FICA_Wages â 125 | = 6596.13 â 200.33 | = 6395.80 |

1) FICA ER â No Self Adjust Method

| PC 7031 FICA ER | = FICA ER Earn x 0.062 | = 6395.80 x 0.062 | = 396.54 |

| PC 7030 Medicare ER | = Med ER Earn x 0.0145 | = 6395.80 x 0.0145 | = 92.74 |

This employee uses âSelf-Adjust methodâ, please see next page.

2) FICA ER â Self Adjust Method

| FIT_Wages.ctd | Usage 6051 Pre FWT Earnings | = 6676.24 |

| FIT_Wages.ytd | Usage 6051 Pre FWT Earnings | = 51747.29 |

| FSP_Wages.ctd | Usage 6055 Pre-FIT Suppl Earns | = 0 |

| FSP_Wages.ytd | Usage 6055 Pre-FIT Suppl Earns | = 5700 |

| FICA_Wages.ctd | Usage 6261 Pre-FICA Employer Earnings | = 6596.13 |

| FICA_Wages.ytd | Usage 6261 Pre-FICA Employer Earnings | = 51057.92 |

If FICA Earnings (FICA_Wages.ctd) is different than FIT Earnings (FIT_Wages.ctd), then calculate the difference between the Wages for FICA and FIT (i.e. Usage 6261 â Usage 6051), called this Additional FICA Wages

| CTD Usage 6261 Pre-FICA Employer Earnings | 6596.13 |

| CTD Usage 6051 Pre FWT Earnings | 6676.24 |

| CTD Addn FICA Wages | 6596.13 â 6676.24 = -80.11 (negative means FICA Earn < Pre-FWT Earn) |

| YTD Usage 6261 Pre-FICA Employer Earnings | 51057.92 |

| YTD Usage 6051 Pre FWT Earnings | 51747.29 |

| YTD Addn FICA Wages | 51057.92 â 51747.29 = -689.37 (negative means FICA Earn < Pre-FWT Earn) |

| Addn FICA_Wages.ctd | = -80.11 FICA.ytdEE | = 3459.44 (dedn so far) MEDI.ytd = 809.06 (dedn so far) |

| Addn FICA_Wages.ytd | = -689.37 FICA.ytdER | = 3459.44 (dedn so far) |

| YTD 125 Total (from YTD) | = 1649.91 (prorate to YTD FIT / FSP Wages, i.e. 51747.29 and 5700) | |

| YTD 401K Total (from YTD) | = 2026.80 (prorate to YTD FIT / FSP Wages, i.e. 51747.29 and 5700) | |

| FIT_ben_125.ctd | = 200.83 FSP_ben_125.ctd | = 0 |

| FIT_ben_125.ytd | = 1486.20 FSP_ben_125.ytd | = 163.71 (1486.20 + 163.71 = 1649.91) |

| FIT_ben_401K.ctd | = 239.57 FSP_ben_401K.ctd | = 0 |

| FIT_ben_401K.ytd | = 1825.70 FSP_ben_401K.ytd | = 201.1 (1825.70 + 201.1 = 2026.80) |

- Calculate FICA Wages for the Year

| FIT_Wages.ctd | + Addn FICA_Wages.ctd | + FIT_Wages.ytd | + Addn FICA_Wages.ytd | |

| 6676.24 | + (-80.11) | + 51747.29 | + (-689.37) | = 57654.05 |

| FSP_Wages.ctd | + FSP_Wages.ytd | |

| 0 | + 5700 | = 5700 |

| FICA_Wages_Total | = 57654.05 + 5700 | = 63354.05 |

- Calculate 125 Exemption for the Year

| FICA_125_Total | = FIT_ben_125.ctd | + FSP_ben_125.ctd | + FIT_ben_125.ytd | + FSP_ben_125.ytd | |

| FICA_125_Total | = 200.83 | + 0 | + 1486.20 | + 163.71 | = 1850.74 |

- FICA ER Calculation

| FICA Taxable Earnings | = FICA_Wages_Total â FICA_125_Total | |

| FICA Taxable Earnings | = 63354.05 â 1850.74 | = 61503.31 |

| FICA ER Contribution | = FICA Taxable Earnings x FICA Rate | |

| FICA ER Contribution | = 61503.31 x 0.062 | = 3813.21 |

| FICA ER YTD so far | = YTD PC 7031 FICA ER + PC 7033 RR Tier1 Soc ER | |

| FICA ER YTD so far | = 1810.19 + 1649.25 | = 3459.44 (FICA.ytdER so far) |

| FICA ER this pay | = FICA ER Contribution â FICA ER YTD so far | |

| FICA ER this pay | = 3813.21 â 3459.44 | = 353.77 (RPREGC slight rounding 353.80) |

- Medicare ER Calculation

| MEDI ER Contribution | = FICA Taxable Earnings x FICA Rate | |

| MEDI ER Contribution | = 61503.31 x 0.0145 | = 891.80 |

| MEDI ER YTD so far | = YTD PC 7030 Medicare ER + PC 7034 RR Tier1 Med ER | |

| MEDI ER YTD so far | = 423.35 + 385.71 | = 809.06 (MEDI.ytd so far) |

| MEDI ER this pay | = MEDI ER Contribution â MEDI ER YTD so far |

Railroad Tax Calculation#

Railroad â Tier1 Tax Example#

US Federal Tax Calculation_03.JPG

| FIT_Wages | Usage 6051 Pre FWT Earnings | 6153.82 |

| RRTA_Wages | Usage 6306 Pre-RR Tier1 SOC ER Earnings | 6079.97 |

| PC 8005 FIT Earn | = FIT Wages â 125 - 401K | = 6153.82 â194.22 â 225.31 | = 5734.29 |

| PC 8201 RR Tier1 Soc ER Earn | = RRTA Wages â 125 | = 6079.97 â194.22 | = 5885.75 |

1)RRTA â No Self Adjust Method

| PC 7033 RR Tier1 Soc ER | = RR Tier1 Earn x 0.062 | = 5885.75 x 0.062 | = 364.92 |

| PC 7034 RR Tier1 Med ER | = RR Tier1 Earn x 0.0145 | = 5885.75x 0.0145 | = 85.34 |

- For Railroad Taxation, if an employee has FICA contribution during the year, this means the employee works between the Railroad and Non-Railroad Assignments. In this case, please check if the âRR Self-Adjustâ Method should be used for this Employee or not.

- The reason is, if âRR Self-Adjustâ method is defined on IPRLU, this method is applicable for both RR Tier1 and Tier2 calculation, but since Regular FICA does not have a Tier2 calculation, the âRR Self-Adjustâ method will automatically re-adjust all Earnings that include YTD FICA Earnings that are not subject to Tier2 calculation, this would cause the entire YTD Earnings to subject to Tier2 tax

- Since employee should only pay Tier2 tax for the Earnings that are earned for Railroad employment, if employee has FICA contribution, the user should verify if this employee should use the âSelf-Adjustâ method to re-calculate all Tier2 tax or just to use âRR No Self-Adjustâ method.

- Next page example shows the âRR Self-Adjust methodâ and should be used when Employee does not have FICA employment

| FIT_Wages.ctd | Usage 6051 Pre FWT Earnings | = 6153.82 |

| FIT_Wages.ytd | Usage 6051 Pre FWT Earnings | = 58423.53 |

| FSP_Wages.ctd | Usage 6055 Pre-FIT Suppl Earns | = 0 |

| FSP_Wages.ytd | Usage 6055 Pre-FIT Suppl Earns | = 5700 |

| RRTA_Wages.ctd | Usage 6306 Pre-Tier1 Soc ER Earn | = 6079.97 |

| RRTA_Wages.ytd | Usage 6306 Pre-Tier1 Soc ER Earn | = 57654.05 |

If RRTA Earnings (RRTA_Wages.ctd) is different than FIT Earnings (FIT_Wages.ctd), then calculate the difference between the Wages for RRTA and FIT (i.e. Usage 6306 â Usage 6051), called this Additional RRTA Wages

| CTD Usage 6306 Pre-Tier1 Soc ER Earn | 6079.97 | |

| CTD Usage 6051 Pre FWT Earnings | 6153.82 | |

| CTD Addn FICA Wages | 6079.97 â 6153.82 | = -73.85 (negative means RRTA Earn < Pre-FWT Earn) |

| YTD Usage 6306 Pre-Tier1 Soc ER Earn | 57654.05 | |

| YTD Usage 6051 Pre FWT Earnings | 58423.53 | |

| YTD Addn FICA Wages | 57654.05 â 58423.53 | -769.48 (negative means RRTA Earn < Pre-FWT Earn) |

| Addn RRTA_Wages.ctd | = -73.85 | RRTA.ytd_Tier1_ER = 3813.24 (dedn so far) |

| Addn RRTA_Wages.ytd | = -769.48 |

| YTD 125 Total (from YTD) | = 1850.24 (prorate to YTD FIT / FSP Wages, i.e. 58423.53 and 5700) | ||

| YTD 401K Total (from YTD) | = 2266.37 (prorate to YTD FIT / FSP Wages, i.e. 58423.53 and 5700) | ||

| FIT_ben_125.ctd | = 194.22 FSP_ben_125.ctd | = 0 | |

| FIT_ben_125.ytd | = 1685.77 FSP_ben_125.ytd | = 164.47 | (1685.77 + 164.47 = 1850.24) |

| FIT_ben_401K.ctd | = 225.31 FSP_ben_401K.ctd | = 0 | |

| FIT_ben_401K.ytd | = 2064.91 FSP_ben_401K.ytd | = 204.46 | (2064.91 + 204.46 = 2269.37) |

- Calculate RRTA Wages for the Year

| FIT_Wages.ctd | + Addn RRTA_Wages.ctd | + FIT_Wages.ytd | + Addn RRTA_Wages.ytd | |

| 6153.82 | + (-73.85) | + 58423.53 | + (-769.48) | = 63734.02 |

| FSP_Wages.ctd | + FSP_Wages.ytd | |

| 0 | + 5700 | = 5700 |

| RRTA_Wages_Total | = 63734.02 + 5700 | = 69434.02 |

- Calculate 125 Exemption for the Year

| RRTA_125_Total | = FIT_ben_125.ctd | + FSP_ben_125.ctd | + FIT_ben_125.ytd | + FSP_ben_125.ytd | |

| RRTA_125_Total | = 194.22 | + 0 | + 1685.77 | + 164.47 | = 2044.46 |

- RRTA Tier1 ER Calculation

| RRTA Taxable Earnings | = RRTA_Wages_Total â RRTA_125_Total | |

| RRTA Taxable Earnings | = 69434.02 â 2044.46 | = 67389.56 |

| RRTA Tier1 ER Contribution | = RRTA Taxable Earnings x RRTA Tier1 ER Rate | |

| RRTA Tier1 ER Contribution | = 67389.56 x 0.062 | = 4178.15 |

| RRTA ER YTD so far | = YTD PC 7031 FICA ER + PC 7033 RR Tier1 Soc ER | |

| RRTA ER YTD so far | = 2163.99 + 1649.25 | = 3813.24 (RRTA.ytdER so far) |

| RRTA Tier1 ER this pay | = RRTA ER Contribution â RRTA ER YTD so far | |

| RRTA Tier1 ER this pay | = 4178.15 â 3813.24 | = 364.81 |

{kind=link}

{kind=link}

{kind=link}