Table of Contents

- US TAXATION SUPPLEMENTAL PAY PROCESSING

- Overview

- Federal Level

- Federal Supplemental Tax Methods

- Prorating Taxable Benefits for Federal Supplemental Pay

- State Level

- State Supplemental Pay

- State Supplemental Tax – WITH or WITHOUT Regular Pay

- IPUTP – Supplemental Tax Method by State

- IPRLU – Supplemental Tax Method by Employee

- Notes

US TAXATION SUPPLEMENTAL PAY PROCESSING#

Overview#

This document describes the US Supplemental Pay Processing that is used in the Symmetry Tax Engine (STE).Federal Level#

Federal Supplemental Tax Methods#

- The Supplemental tax for Federal withholding is computed using the federal percentage (i.e. 25% of wages on the first $1,000,000 in supplemental wages and 35% of wages on any amount over $1,000,000).

- At Employee level on IPRLU, the employee specifies the employee’s Federal Supplemental Tax Method that determines if the Supplemental tax should be calculated for this employee

- If Federal Supplemental tax is to be calculated for an employee, UPCALC will internally pass the ‘FLAT’ Percentage Method to Symmetry that will calculate FSP Tax using the federal 25% or 35%

- Regardless if the Supplemental Wages are paid WITH or WITHOUT the Regular Wages, Federal Supplemental tax is calculated using this ‘FLAT’ Percentage Method by Symmetry

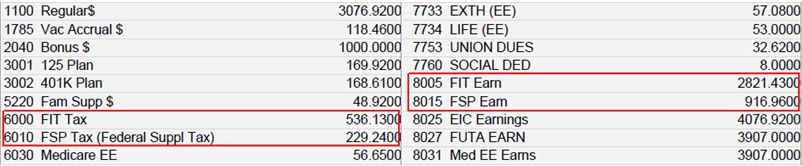

For Example: Sup is Paid with Regular Wages, when FSP Method = ‘Flat Percent Method’

US_Taxation _Supplemental Pay Processing_01.JPG

PC 6010 FSP Tax 916.96 x 25%= 229.24

Prorating Taxable Benefits for Federal Supplemental Pay#

When a supplemental pay is paid with a regular pay, the taxable benefit deductions may be prorated between both Federal wages and Supplemental wages. This is controlled by the set up of elements attached to specific pay components as indicated below.

Prorating the taxable benefit deductions will cause a slight difference in the tax calculated. Clients will need to consider their business processes to determine if they would prefer the taxable benefits to be prorated or not. Some clients may want to prorate section 125 deductions and not 401k deductions.

UPCALC reviews the set up of the following Federal PC Usages to determine if it should prorate the taxable benefit deductions:

| 6053 - Pre-FWT 125 Exemption - Regular Tax (PPE) |

| 6054 - Pre-FWT 401K Exemption - Regular Tax (PPE) |

| 6056 - Pre-FWT 125 Exemption - Supplemental Tax (PPE) |

| 6057 - Pre-FWT 401K Exemption - Supplemental Tax (PPE) |

The proration logic will occur when:

- No Supplemental Element is associated to the Supplemental PC Usages listed above (i.e. 6056, 6057), UPCALC will prorate all of the section 125 and 401k deduction amounts between Regular and Supplemental

- A Supplemental Element has been associated to the Supplemental PC Usages listed above, the Element is defined with PCs and those PCs have amounts, UPCALC will use the Element and prorate the taxable benefits defined in the element.

The proration logic will NOT occur when:

- A Supplemental Element has been associated to the Supplemental PC Usages but the Element is Empty (no PCs defined).

- A Supplemental Element has been associated to the Supplemental PC Usages but the PCs within the Element do not have amounts in the pay.

Set Up Options to Prorate Section 125 Taxable Benefits between Federal and Supplemental:

- In IPPC do not associate an element to PC Usage 6056 - Pre-FWT 125 Exemption - Supplemental Tax (PPE).This will cause UPCALC to prorate all of the section 125 taxable benefit deductions that are defined in the element tied to PC Usage 6053 Pre-FWT 125 Exemption - Reg Tax (PPE).

- If only certain Sect 125 deductions should be prorated, define an element in IPPE that only lists the 125 deductions that should be prorated between Federal and Supplemental. In IPPC attach this element to the Pay Component tied to PC Usage6056 - Pre-FWT 125 Exemption - Supplemental Tax (PPE)

Set up Options to Prorate 401k Taxable Benefits between Federal and Supplemental:

- In IPPC do not associate an element to PC Usage 6057 - Pre-FWT 401K Exemption - Supplemental Tax (PPE). This will cause UPCALC to prorate all of the 401k/457 taxable benefit deductions that are defined in the element tied to 6054 Pre-FWT 401K Exemption - Reg Tax (PPE)

- If only certain 401k or 457 deductions should be prorated between Federal and Supplemental, define an element in IPPE that only lists the 401k and 457 deductions that should be prorated. In IPPC attach this element to the Pay Component tied to PC Usage 6057 - Pre-FWT 401K Exemption - Supplemental Tax (PPE)

After UPCALC or Trial Calc, on IPPH ‘PAY JURISDICTION’ Tab, user can click the Jurisdiction ’00-000-0000 Federal’ entry and scroll down the ‘Tax Identifier’ list, the prorated 125 and 401K amounts are stored for these Benefit usages with description ‘Pre-FWT 125 Exemption - Supplemental Tax (PPE)’ etc.

The following is an example of proration:

| PC 1010 Regular Earnings | 2307.6900 |

| PC 2002 Bonus $ | 1000.0000 |

| PC 4020 Medical EE (sect125) | 50.0000 |

| PC 4041 401K Dedn | 33.0800 |

| PC 6000 Fed Tax | 393.2000 |

| PC 6003 Fed Supp Tax | 243.7200 |

| PC 8000 Fed Tax Earns | 2249.7300 |

| PC 8010 Fed Sup Earns | 974.8800 |

| PC 6055 Res SIT Tax | 138.0000 |

| PC 6057 Res Supp Tax | 61.0000 |

| PC 8055 Res SIT Earn | 2249.7300 |

| PC 8058 Res Supp Earn | 974.8800 |

| PC 8400 Pre-Fed Earnings | 2307.6900 |

| PC 8403 Pre-Fed Sup Ern | 1000.0000 |

| PC 8153 Pre Fed 125 Earn | 34.8800 |

| PC 8154 Pre Fed 401 Earn | 23.0800 |

| PC 8156 Pre Fed Sup 125 | 15.1200 |

| PC 8167 Pre FSP 401 Earn | 10.0000 |

| PC 8551 Pre-SIT Earnings | 2307.6900 |

| PC 8453 Pre-SIT Suppl Earns | 1000.0000 |

| PC 8353 Pre-SIT 125 | 34.8800 |

| PC 8354 Pre-SIT 401/403/457 | 23.0800 |

| PC 8356 Pre-SIT Supp 125 | 15.1200 |

| PC 8357 Pre-SIT Supp 401K | 10.0000 |

UPCALC prorated both sect 125 and 401k taxable benefits against regular and supplemental wages for Federal and State.

PC 4020 Medical EE (sect125) $50.0000

| PC 8153 Pre Fed 125 Earn | 34.8800 prorated amt on reg wages |

| PC 8156 Pre Fed Sup 125 | + 15.1200 prorated amt on supp wages |

| 50.00 |

PC 4041 401K Dedn $33.0800

| PC 8154 Pre Fed 401 Earn | 23.0800 prorated amt on reg wages |

| PC 8167 Pre FSP 401 Earn | + 10.0000 prorated amt on supp wages |

| 33.08 |

The Pre-Fed Earnings are reduced accordingly:

| Pre-Fed Earnings | 2307.6900 |

| Pre Fed 125 Earn | -34.8800 |

| Pre Fed 401 Earn | -23.0800 |

| Fed Tax Earns | 2249.7300 |

The Pre-Fed Supp Earnings are reduced accordingly:

| Pre-Fed Sup Ern | 1000.0000 |

| Pre Fed Sup 125 | - 15.1200 |

| Pre FSP 401 Earn | - 10.0000 |

| Fed Sup Earns | 974.8800 |

The FIT Tax is based on $2249.73 The FSP Tax is based on $974.88

On IPPH ‘PAY JURISDICTION’ tab, user can click the Jurisdiction ’00-000-0000 Federal’ entry and scroll down the ‘Tax Identifier’ list, the prorated 125 and 401K amounts are stored as ‘Pre-FWT 125 Exemption - Supplemental Tax (PPE)’ etc.

The following is an example of the same pay, without proration:

| PC 1010 Regular Earnings | 2307.6900 |

| PC 2002 Bonus $ | 1000.0000 |

| PC 4020 Medical EE (sect125) | 50.0000 |

| PC 4041 401K Dedn | 33.0800 |

| PC 6000 Fed Tax | 386.9200 |

| PC 6003 Fed Supp Tax | 250.0000 |

| PC 6055 Res SIT Tax | 136.0000 |

| PC 6057 Res Supp Tax | 63.0000 |

| PC 8000 Fed Tax Earns | 2224.6100 |

| PC 8010 Fed Sup Earns | 1000.0000 |

| PC 8055 Res SIT Earn | 2224.6100 |

| PC 8058 Res Supp Earn | 1000.0000 |

| PC 8400 Pre-Fed Earnings | 2307.6900 |

| PC 8403 Pre-Fed Sup Ern | 1000.0000 |

| PC 8153 Pre Fed 125 Earn | 50.0000 |

| PC 8154 Pre Fed 401 Earn | 33.0800 |

| PC 8551 Pre-SIT Earnings | 2307.6900 |

| PC 8453 Pre-SIT Suppl Earns | 1000.0000 |

| PC 8353 Pre-SIT 125 | 50.0000 |

| PC 8354 Pre-SIT 401/403/457 | 33.0800 |

UPCALC did not prorate the sect 125 or 401k deductions against regular and supplemental wages.

The Pre-Fed Earnings are reduced accordingly:

| Pre-Fed Earnings | 2307.6900 |

| Pre Fed 125 Earn | -50.0000 |

| Pre Fed 401 Earn | -33.0800 |

| Fed Tax Earns | 2224.6100 |

The Pre-Fed Supp Earnings are not reduced since the sect 125 and 401k taxable benefits were not prorated. Pre-Fed Sup Ern 1000.0000

The FIT Tax is based on $2224.6100 The FSP Tax is based on $1000.0000

State Level#

State Supplemental Pay#

- At the State Level, Symmetry Tax Engine uses the following tax methods to calculate tax on supplemental wages: **Flat

- Current Aggregation

- Previous Aggregation

- UPCALC needs to pass one of these Supplemental Tax Methods to the Symmetry Tax Engine

- For State that has a specific Supplemental Flat percentage, the ‘Flat Rate Method’ can be used

- Not all States have a specific flat percentage for Supplemental wages, for these States, the ‘Current Aggregation’ method should be used.

- The current aggregation method adds the regular wages to the supplemental wages and computes withholding using the annualized method on the combined total. The difference between the withholding on the combined total (regular and supplemental) and the withholding on regular wages is the supplemental wage withholding.

- The ‘Previous Aggregation’ Method will not be supported until there is a need to use this method

- On next page, a list is shown for States that are with and without the Supplemental Tax Percent

- From this list, the following sStates do not supply a Flat percent and therefore the ‘Current Aggregation’ method is used in order to calculate State Sup Tax:

AK, AZ, CT, DE, FL, HI, KY, LA, MA, MD, MS, NH, NJ, SD, TN, TX, UT, WA, WY, PR - From this list, the remaining states will use the ‘Flat’ method in order to calculate State Sup Tax

- From this State list, the Default Supplemental Tax Method is set for each State internally by the System

- Depending on if the Supplemental Wages are paid WITH or WITHOUT the Regular Wages, each State may provide different method to calculate the State Supplemental Tax, please read below

- At Employee level on IPRLU, the employee will specify the State Supplemental Tax Method that determines if the Supplemental tax is to be calculated for this employee for a pay

- If State Supplemental tax is to be calculated by Symmetry, then the Default Sup Tax Method of ‘Flat’ or ‘Current Aggregation’ method will be passed to Symmetry

- On IPTUP for each State, the user can manually override the default Supplemental Tax Method to ‘FLAT’ or ‘CURRAGG’ depending on if the users prefer to tax by which method, then on IPRLU State Miscellaneous Tab, employee may override this State level default Supplemental tax method

The following table lists the States that are with and without the Supplemental Tax Percent as of Sept 2006.

US_Taxation _Supplemental Pay Processing_02.JPG

State Supplemental Tax – WITH or WITHOUT Regular Pay#

- Depending on if the Supplemental Wages are paid WITH or paid WITHOUT the Regular Wages, each State may have different methods to handle Supplemental taxes. Please refer to this link:

http://www.payroll-taxes.com/PayrollTaxes/supplemental_states.htm

An Example for the State of Maryland below shows the differences of the State Supplemental Tax results when the ‘FLAT’ or ‘CURRAGG’ tax methods are used.

| Maryland GEO: 24-001-1713506 Allegany | |

| Paid with Regular Wages | Paid at Different Time than Regular Wages |

| Add to regular wages and Withhold on total | Withhold at 6.25% plus rate applicable to county of residence Or Add to regular wages, compute tax on total, and Subtract tax withheld on regular wages |

- Local Level Supplemental Tax Method uses the same State Level Supplemental Tax Method

For Example: State of Maryland:- Supplemental is Paid with Regular Wages, when SSP Method = ‘Flat Percent Method’

- this actually uses Method ‘Paid at Different Time than Regular Wages’

US_Taxation _Supplemental Pay Processing_03.JPG

Maryland Sup Rate 916.96 x 6.25% = 57.31

Local Rate for Allegany County, MD 916.96 x 0.0305 = 27.97

= 85.28: PC 6052

Res SIT + Res Supp Tax 214.07 + 85.28 = 299.35

Note: Higher than ‘CURRAGG’ method

- this actually uses Method ‘Paid at Different Time than Regular Wages’

- Sup is Paid with Regular Wages, when SSP Method = ‘Current Aggregation’

US_Taxation _Supplemental Pay Processing_04.JPG

Res SIT + Res Supp Tax 214.07 + 71.52 = 285.59

Note: same result as Vertex below - Sup is Paid with Regular Wages, Vertex Supplemental tax for Maryland:

US_Taxation _Supplemental Pay Processing_05.JPG

Work SIT = Res SIT + Res Supp Tax = 285.59

- Supplemental is Paid with Regular Wages, when SSP Method = ‘Flat Percent Method’

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

In Conclusion for Maryland:

- When Sup is paid WITH Regular Wages, the ‘Current Aggregation’ method should be used

- When Sup is paid WITHOUT Regular Wages, the ‘Current Aggregation’ or ‘Flat’ method can be used

IPUTP – Supplemental Tax Method by State#

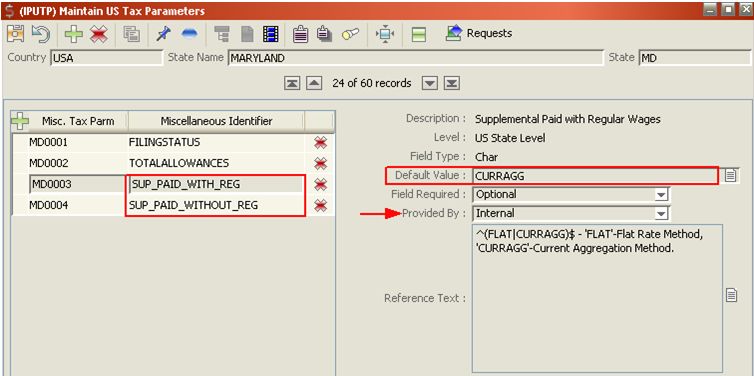

- when UPUTR is run, UPUTR automatically loads in two Miscellaneous Identifiers for each State to provide the Default Supplemental Tax Method:

SUP_PAID_WITH_REG

SUP_PAID_WITHOUT_REG

{kind=link}

- Default Value

-this contains ‘FLAT’ or ‘CURRAGG’ depending on each State

- Provided By

-always ‘Internal’

-when UPCALC is passing State Misc Parms to Symmetry, UPCALC will not pass the State Misc Parm that are with ‘Provided By’ = ‘Internal’

- in UPCALC, if an employee is paid Supplemental Wages with the Regular Wages in the same pay, then the ‘SUP_PAID_WITH_REG’ Default Value will be used

- in UPCALC, if an employee is paid Supplemental Wages without the Regular Wages in the same pay, then the ‘SUP_PAID_WITHOUT_REG’ Default Value will be used

IPRLU – Supplemental Tax Method by Employee#

- at employee level, the employee may optionally override the default State Sup Tax Method on IPUTP for:

SUP_PAID_WITH_REG

SUP_PAID_WITHOUT_REG - if there is no override by employee, there is no need to set up these Misc Tax Parm

- for IPRLU Federal and State Tab Suppl Tax Method explanation, please refer to: PR_US_IPRLU_methods_v1.0.doc or later

- when an employee is paid with Supplemental wages, the IPRLU Federal and State Tab Suppl Tax Method determines if the Supplemental Wages are to be taxed or not, and which Suppl Tax Method is to be used

- once when the State Supplemental tax is to be calculated by Symmetry, then IPUTP State specific tax method from SUP_PAID_WITH_REG or SUP_PAID_WITHOUT_REG will be passed to Symmetry for calculation depending on if the Supplemental wages are paid with or without Regular wages, therefore FLAT or CURRAGG is passed

3.5 Prorating Taxable Benefits for State Supplemental Pay

Like with the Federal Supplemental Pay, taxable benefits may be prorated between regular state wages and supplemental wages when both are paid together. This is controlled by the set up of elements attached to specific pay components as indicated below.

Prorating the taxable benefit deductions will cause a slight difference in the tax calculated. Clients will need to consider their business processes to determine if they would prefer the taxable benefits to be prorated or not. Some clients may want to prorate section 125 deductions and not 401k deductions.

UPCALC reviews the set up of the following State PC Usages to determine if it should prorate the taxable benefit deductions: If the State Level Benefit PC Usages are not set up on IPPC, then the Federal Level Benefit PC Usages that are described in the Federal section will be used.

6653 - Pre-State 125 Exemption - Regular Tax (PPE) 6654 - Pre-State 401 Exemption - Regular Tax (PPE) 6656 - Pre-State 125 Exemption - Supplemental Tax (PPE) 6657 - Pre-State 401 Exemption - Supplemental Tax (PPE)

The proration logic will occur when: No Supplemental Element is associated to the Supplemental PC Usages listed above, UPCALC will prorate all of the section 125 and 401k deduction amounts between Regular and Supplemental A Supplemental Element has been associated to the Supplemental PC Usage, the Element is defined with PCs and those PCs have amounts, UPCALC will use the Element and prorate the taxable benefits defined in the element.

The proration logic will NOT occur when: A Supplemental Element has been associated to the Supplemental PC Usages listed above but the Element is Empty (no PCs defined). A Supplemental Element has been associated to the Supplemental PC Usages listed above but the PCs within the Element do not have amounts in the pay.

Set Up Options to Prorate Section 125 Taxable Benefits between State Regular Wages and Supplemental: 1. In IPPC do not associate an element to PC Usage 6656 - Pre-State 125 Exemption - Supplemental Tax (PPE). This will cause UPCALC to prorate all of the section 125 taxable benefit deductions that are defined in the element tied to PC Usage 6653 Pre-State 125 Exemption - Regular Tax (PPE). 2. If only certain Sect 125 deductions should be prorated, define an element in IPPE that only lists the 125 deductions that should be prorated between Federal and Supplemental. In IPPC attach this element to the Pay Component tied to PC Usage 6656 - Pre-State 125 Exemption - Supplemental Tax (PPE)

Set up Options to Prorate 401k Taxable Benefits between Federal and Supplemental: 1. In IPPC do not associate an element to PC Usage 6657 - Pre-State 401 Exemption - Supplemental Tax (PPE). This will cause UPCALC to prorate all of the 401k/457 taxable benefit deductions that are defined in the element tied to PC Usage 6654 Pre-State 401 Exemption - Regular Tax (PPE) 2. If only certain 401k or 457 deductions should be prorated between Federal and Supplemental, define an element in IPPE that only lists the 401k and 457 deductions that should be prorated. In IPPC attach this element to the Pay Component tied to PC Usage 6657 - Pre-State 401 Exemption - Supplemental Tax (PPE)

After UPCALC or Trial Calc, on IPPH ‘PAY JURISDICTION’ Tab, user can click the Jurisdiction entry for the appropriate Jurisdiction name and scroll down the ‘Tax Identifier’ list, the prorated 125 and 401K amounts are stored for these Benefit usages with description ‘Pre-State 125 Exemption - Reg Tax (PPE)’ etc.

The following is an example of proration:

PC 1010 Regular Earnings 2307.6900 PC 2002 Bonus $ 1000.0000 PC 4020 Medical EE (sect125) 50.0000 PC 4041 401K Dedn 33.0800 PC 6000 Fed Tax 393.2000 PC 6003 Fed Supp Tax 243.7200 PC 8000 Fed Tax Earns 2249.7300 PC 8010 Fed Sup Earns 974.8800 PC 6055 Res SIT Tax 138.0000 PC 6057 Res Supp Tax 61.0000 PC 8055 Res SIT Earn 2249.7300 PC 8058 Res Supp Earn 974.8800 PC 8400 Pre-Fed Earnings 2307.6900 PC 8403 Pre-Fed Sup Ern 1000.0000 PC 8153 Pre Fed 125 Earn 34.8800 PC 8154 Pre Fed 401 Earn 23.0800 PC 8156 Pre Fed Sup 125 15.1200 PC 8167 Pre FSP 401 Earn 10.0000 PC 8551 Pre-SIT Earnings 2307.6900 PC 8453 Pre-SIT Suppl Earns 1000.0000 PC 8353 Pre-SIT 125 34.8800 PC 8354 Pre-SIT 401/403/457 23.0800 PC 8356 Pre-SIT Supp 125 15.1200 PC 8357 Pre-SIT Supp 401K 10.0000

UPCALC prorated both the sect 125 and 401k taxable benefits against regular and supplemental wages for both Federal and State.

PC 4020 Medical EE (sect125) $50.0000 PC 8353 Pre-SIT 125 34.8800 prorated amt on reg wages PC 8356 Pre-SIT Supp 125 + 15.1200 prorated amt on supp wages 50.00

PC 4041 401K Dedn $33.0800 PC 8354 Pre-SIT 401/403/457 23.0800 prorated amt on reg wages PC 8357 Pre-SIT Supp 401K + 10.0000 prorated amt on supp wages 33.08

The Pre-State Earnings are reduced accordingly: Pre-SIT Earnings 2307.6900 Pre-SIT 125 - 34.8800 Pre-SIT 401/403/457 - 23.0800 RES SIT Earns 2249.7300

The Pre-Fed Supp Earnings are reduced accordingly: Pre-SIT Suppl Earns 1000.0000 Pre-SIT Supp 125 - 15.1200 Pre-SIT Supp 401K - 10.0000 Fed Sup Earns 974.8800

The SIT Tax is based on $2249.73 The SSP Tax is based on $974.88

The following is an example of the same pay, without proration:

PC 1010 Regular Earnings 2307.6900 PC 2002 Bonus $ 1000.0000 PC 4020 Medical EE (sect125) 50.0000 PC 4041 401K Dedn 33.0800 PC 6000 Fed Tax 386.9200 PC 6003 Fed Supp Tax 250.0000 PC 6055 Res SIT Tax 136.0000 PC 6057 Res Supp Tax 63.0000 PC 8000 Fed Tax Earns 2224.6100 PC 8010 Fed Sup Earns 1000.0000 PC 8055 Res SIT Earn 2224.6100 PC 8058 Res Supp Earn 1000.0000 PC 8400 Pre-Fed Earnings 2307.6900 PC 8403 Pre-Fed Sup Ern 1000.0000 PC 8153 Pre Fed 125 Earn 50.0000 PC 8154 Pre Fed 401 Earn 33.0800 PC 8551 Pre-SIT Earnings 2307.6900 PC 8453 Pre-SIT Suppl Earns 1000.0000 PC 8353 Pre-SIT 125 50.0000 PC 8354 Pre-SIT 401/403/457 33.0800

UPCALC did not prorate the sect 125 or 401k deductions against regular and supplemental wages.

The Pre-State Earnings are reduced accordingly: Pre-SIT Earnings 2307.6900 Pre-SIT 125 - 50.0000 Pre-SIT 401/403/457 - 33.0800 RES SIT Earns 2224.6100

The Pre-SIT Supplemental Earnings are not reduced since the sect 125 and 401k taxable benefits were not prorated. Pre-SIT Suppl Earns $1000.0000

The SIT Tax is based on $2224.6100 The SSP Tax is based on $1000.0000

Notes #

Click to create a new notes pageScreen captures are meant to be indicative of the concept being presented and may not reflect the current screen design.

If you have any comments or questions please email the Wiki Editor

All content © High Line Corporation