Table of Contents

- UPCALC INSUFFICIENT EARNINGS

- Overview

- Normal Earnings Pay Point

- IPPP – Pay Point Set Up

- UPCALC – Insufficient Earnings Example

- Insufficient Earnings Pay Point

- IPPP – Insufficient Earnings Pay Point Set Up

- UPCALC – After Insufficient Earnings Pay Point processing

- Insufficient Earnings Pay Point Processing

- UPCALC – Insufficient Earnings Pay Point Processing

- Notes

UPCALC INSUFFICIENT EARNINGS#

Overview#

The system allows you to handle an insufficient earnings situation where employees do not have enough earnings to cover all their deductions. This section explains how to set up the Pay Point Table (IPPP) in order to perform or re-calculate certain Pay Point tasks during the Net Pay Calculation process to adjust the net pay amount in UPCALC.Normal Earnings Pay Point#

IPPP – Pay Point Set Up#

For normal regular processing in UPCALC, the following Pay Point set up is usually used to define Net Pay after Legislative Calculation.

UPCALC Insufficient Earnings_01.JPG

{kind=link}

When the employee’s gross earnings are not enough to cover all deductions, this time sheet will trigger the Insufficient Earnings processing logic.

For each deduction pay component, the IPPC Acct/Arrears tab must indicate the actions to be taken for this deduction.

If the deduction is an exemption amount to reduce the taxable earnings, and the full deduction amount is not taken, then the taxable earnings will be in an incorrect situation, please see next section for an example.

UPCALC – Insufficient Earnings Example#

UPCALC Insufficient Earnings_02.JPG{kind=link}

From this pay, before Net Pay calculation, the following pay component values are:

| PC 3001 125 Plan | 124.47 |

| PC 3002 401K Plan | 62.56 (original amount) |

For US Taxation, 125 Plan and 401K Plan deductions are to be exempted from Taxable Earnings as follows:

| PC | Gross – 125 Plan – 401K | Total |

|---|---|---|

| PC 8005 FIT Earn | 192.31 – 124.47 – 62.56 | = 5.28 |

| PC 8037 FICA EE Earn | 192.31 – 124.47 | = 67.84 |

| PC 8045 Work SIT Earn | 192.31 – 124.47 – 62.56 | = 5.28 |

From PC 8045 Work SIT Earn of $5.28, it calculates:

| PC 6040 Work SIT | = 0.04 |

From the Net Pay calculation, there is insufficient earnings to cover all deductions. PC 3001 from the IPPC set up is to take as much as possible and generate arrears. Therefore, PC 3001 generated an arrears of 0.96 and PC 3001 is adjusted to 61.60.

For US Taxation, 125 Plan and 401K Plan deductions should be exempted from Taxable Earnings as follows:

| PC | Gross – 125 Plan – 401K | Total |

|---|---|---|

| PC 8005 FIT Earn | 192.31–124.47 – 61.60 | = 5.28 s/b 6.24 |

| PC 8037 FICA EE Earn | 192.3 – 124.47 | = 67.84 |

| PC 8045 Work SIT Earn | 192.31 – 124.47 – 61.60 | = 5.28 s/b 6.24 |

Therefore the above Pay Register results are incorrect.

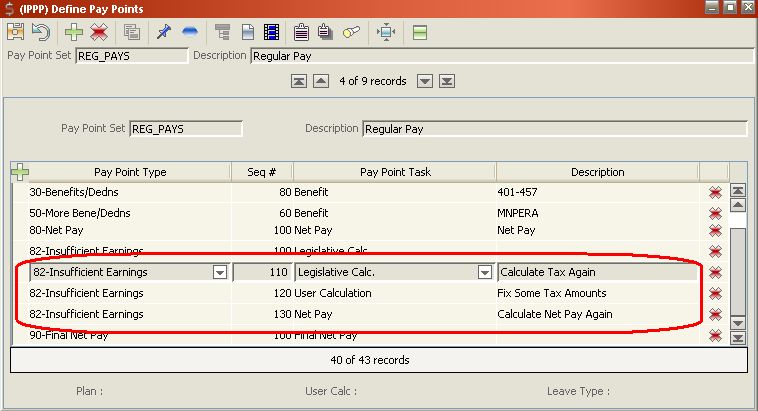

Insufficient Earnings Pay Point#

IPPP – Insufficient Earnings Pay Point Set Up#

When there is are insufficient earnings for an employee, if there are deductions that reduce the taxable earnings, you need to re-calculate taxes again with the adjusted deductions, otherwise the taxable earnings are inflated with the deduction amounts that are not deducted.

On the IPPP screen, the Pay Point Type ‘82-Insufficient Earnings’ is used to specify the Pay Point tasks that are to be performed only when the time sheet is in Insufficient Earnings.

The following is an example for IPPP Insufficient Earnings set up:

UPCALC Insufficient Earnings_03.JPG

{kind=link}

- In ‘82-Insufficient Earnings’ Pay Point, the user can only set up the following Pay Point Tasks:

- Legislative Calc

- User Calculation

- Net Pay

- For US payroll, the Legislative Calc will call the Vertex module again with the revised 125 plan, 401K plan deduction amounts with all earnings for re-calculation

- For Canada, (will update later, only need to call Taxation, not EI, CPP etc. new Pay Point Task?)

- After Legislative Calculation, you may adjust certain tax results base on the client’s own situation, in this case, you need to perform User Calculation to adjust tax amount manually.

e.g. for US Ohio School District tax, you may only withhold School District tax and do not withhold City Residence tax, however, City Residence tax are returned by Vertex in order to calculate the School District tax, then you need to zero out the City Residence tax after taxation.

- After Legislative Calculation, you MUST set up an entry with Pay Point task ‘Net Pay’ to re-calculate Net pay again

UPCALC – After Insufficient Earnings Pay Point processing#

UPCALC Insufficient Earnings_04.JPG

{kind=link}

From first UPCALC, the following pay component values are:

| PC 3001 125 Plan | 124.47 |

| PC 3002 401K Plan | 62.56 61.60 with arrears of 0.96 |

For US Taxation, 125 Plan and 401K Plan deductions are to be exempted from Taxable Earnings as follows:

| PC | Gross – 125 Plan – 401K | Total |

|---|---|---|

| PC 8005 FIT Earn | 192.31 – 124.47 – 61.60 | = 6.24 |

| PC 8037 FICA EE Earn | 192.31 – 124.47 | = 67.84 |

| PC 8045 Work SIT Earn | 192.31 – 124.47 – 61.60 | = 6.24 |

From PC 8045 Work SIT Earn of 5.28 $6.24, it calculates:

| PC 6040 Work SIT | =0.04 0.05 |

When Net Pay is calculated again after taxation, since PC 6040 Work SIT increases from 0.04 to 0.05, there is new Insufficient Earnings for 0.01 (one cent). Therefore PC 3001 generated an additional Arrears 0.01 to 0.97 and PC 3001 is reduced to 61.59, thus the Taxable Earnings need to be adjusted again.

For US Taxation, 125 Plan and 401K Plan deductions should be exempted from taxable earnings as

| Pay Component | Gross – 125 Plan – 401K | Total |

|---|---|---|

| PC 8005 FIT Earn | 192.31 – 124.47 – 61.59 | = 5.28 6.24 to 6.25 |

| PC 8037 FICA EE Earn | 192.31 – 124.47 | = 67.84 |

| PC 8045 Work SIT Earn | 192.31 – 124.47 – 61.59 | = 5.28 6.24 to 6.25 |

US Taxation is called again and all taxable earnings are correct, arrears are generated.

Insufficient Earnings Pay Point Processing#

UPCALC – Insufficient Earnings Pay Point Processing#

- UPCALC processes all Pay Points and Pay Point Tasks according to the IPPP set up for the Pay Category of each time sheet.

- In IPPP ‘80-Net Pay’ Pay Point, if there is insufficient earnings for a time sheet to cover all deductions, UPCALC triggers the Insufficient Earnings logic to generate arrears.

- If any arrears are generated for a time sheet, UPCALC will perform Insufficient Earnings Net Pay Processing according to IPPP ’82-Insufficient Earnings’ pay point set up.

- From IPPP ’82-Insufficient Earnings’ pay point, UPCALC performs the Pay Point Task entries for this Pay Point and then re-check if additional arrears are generated.

- If no more arrears are generated after ’82-Insufficient Earnings’, then UPCALC returns to IPPP Pay Point that is immediately after the ‘80-Net Pay’ Pay Point entry.

- If additional arrears are generated after ’82-Insufficient Earnings’, then UPCALC will perform the same ’82-Insufficient Earnings’ pay point tasks the second time, this is the example as shown above that fix the Taxable Earnings.

- UPCALC will perform ’82-Insufficient Earnings’ pay point entries two times or when there is no arrears generated after the first time is performed.

- The taxation amounts and earnings should be accurate after two recursive calls to ’82-Insufficient Earnings’.

- In IPPP ’82-Insufficient Earnings’ pay point, you may perform the following Pay Point Tasks:

- Legislative Calc

- if any deduction pay components are to be exempted from Taxable Earnings, user must set up Legislative Calc’ entry to re-calc, otherwise not needed

- UserCalc

- user may adjust Tax results after Legislative Calc

- user may adjust Employer portion for Employee Amount

- otherwise not needed

- Net Pay

- if the Tax is re-calculated, then Net Pay Entry must exist

- if user only adjust certain Pay Components that do not affect Net Pay, then there is no need to set up Net Pay entry

- Legislative Calc

- When UPCALC performs ’82-Insufficient Earnings’ pay point, if there are advances given in the same time sheet, UPCALC clears all advances prior to perform ’82-Insufficient Earnings’ pay point because when Net Pay is called again, the advances will be given again.

- When UPAUDT is run to prepare all Pay Point entries for a time sheet, the IPPP ’82-Insufficient Earnings’ entries will not be pulled in by the Prep process in UPAUDT.

- User can set up IPPP ’82-Insufficient Earnings’ pay point by Pay Category, this allows you to dynamically adjust the Net Pay based on the types of pay.

Notes #

Click to create a new notes pageScreen captures are meant to be indicative of the concept being presented and may not reflect the current screen design.

If you have any comments or questions please email the Wiki Editor

All content © High Line Corporation